Renting Out Your Commercial Space? Know Your Risks

.png) Leasing your property can be a great way to generate steady income, but many landlords underestimate the risks that come with it. Spotting

those early makes it easier to protect both your building and your cash flow.

Leasing your property can be a great way to generate steady income, but many landlords underestimate the risks that come with it. Spotting

those early makes it easier to protect both your building and your cash flow.

Damage & Liability Aren’t Tenant Responsibilities

Even with tenants in place, landlords usually carry responsibility for building damage, liability if someone is injured on-site, loss of rental income, theft, and issues like broken glass.

Relying on a tenant’s policy to cover those exposures is unreliable; in most cases, it won’t.

Your own policy should clearly cover property damage, income protection, and third-party claims.

Fact sheets from the Insurance Council of Australia 2025 show that in the past 12 months, property damage and liability still accounted for over half of SME-related claims.

CAUTION

As many as one in five Australian SMEs are underinsured when it comes to building replacement or lost income, according to the Insurance Council. With construction and repair costs having risen sharply in recent years, regular policy reviews are essential to make sure your cover matches the true value and risk profile of your property

Tenant Default and Rent-Loss Safeguards

Current product updates from insurers reveal how rent-default protection is evolving.

Some policies now cover up to a year of lost rent and provide extras like equipment breakdown. For landlords, that kind of protection can mean the difference between stable cash flow and months of lost income if a tenant walks away.

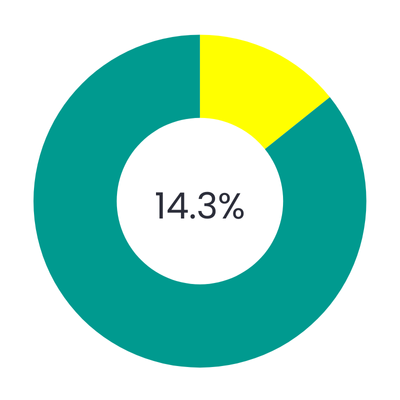

National office vacancies climbed to a 30-year high in mid-2025, averaging 14.3% across CBDs and exceeding 17% in some suburban precincts, according to the Property Council of Australia. Sydney and Melbourne remain elevated, underlining the income risks commercial landlords continue to face.

As well as vacancy rates, be mindful that about one in nine new Aussie SMEs cease trading in their first year.

.png)